If you’re planning to buy your first home, then you’re probably focused on saving for all the costs involved in such a big purchase. One of the expenses that may be at the top of your mind is your down payment. If you’re intimidated by how much you need to save for that, it may be because you believe you must put 20% down. That doesn’t necessarily have to be the case. As the National Association of Realtors (NAR) notes:

“One of the biggest misconceptions among housing consumers is what the typical down payment is and what amount is needed to enter homeownership.”

And a recent Freddie Mac survey finds:

“. . . nearly a third of prospective homebuyers think they need a down payment of 20% or more to buy a home. This myth remains one of the largest perceived barriers to achieving homeownership.”

Here’s the good news. Unless specified by your loan type or lender, it’s typically not required to put 20% down. This means you could be closer to your homebuying dream than you realize.

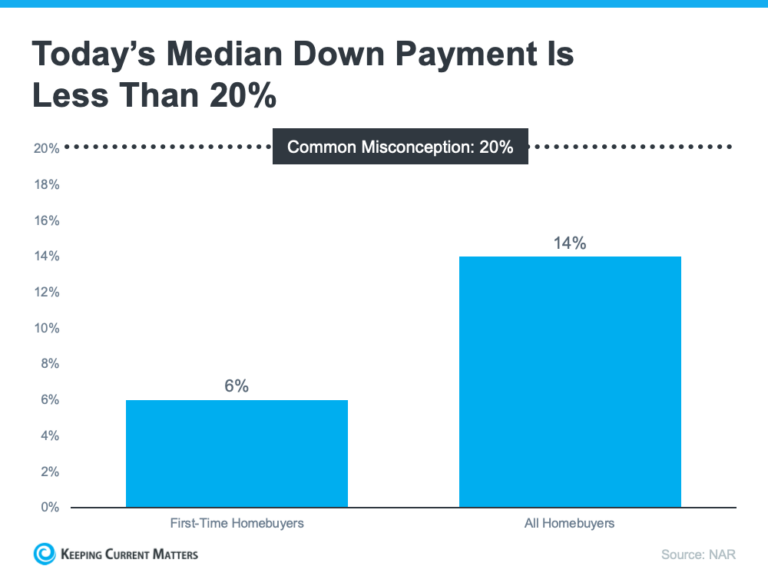

According to NAR, the median down payment hasn’t been over 20% since 2005. In fact, the median down payment for all homebuyers today is only 14%. And it’s even lower for first-time homebuyers at just 6% (see graph below):

What does this mean for you? It means you may not need to save as much as you originally thought.

And it’s not just how much you need for your down payment that isn’t clear. There are also misconceptions about down payment assistance programs. For starters, many people believe there’s only assistance available for first-time homebuyers. While first-time buyers have many options to explore, repeat buyers have some, too.

According to Down Payment Resource, there are over 2,000 homebuyer assistance programs in the U.S., and the majority are intended to help with down payments. That same resource goes on to say:

“You don’t have to be a first-time buyer. Over 38% of all programs are for repeat homebuyers who have owned a home in the last 3 years.”

Plus, there are even loan types, like FHA loans with down payments as low as 3.5% as well as options like VA loans and USDA loans with no down payment requirements for qualified applicants.

If you’re interested in learning more about down payment assistance programs, information is available through sites like Down Payment Resource. Then, partner with a trusted lender to learn what you qualify for on your homebuying journey.

It’s important to dispel the myth that a 20% down payment is always necessary when buying a home. While a larger down payment can have advantages, it is not the only path to homeownership. If you’re eager to purchase a home this year, don’t hesitate to reach out to me. Together, we can start a conversation about your specific homebuying goals and explore the various options available to make your dream a reality. Remember, with the right guidance and tailored financial solutions, you can take confident steps towards becoming a homeowner.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

As millennials enter the housing market, they often face unique challenges compared to previous generations. However, with careful planning and informed decision-making, millennials can overcome these obstacles and embark on the rewarding journey of homeownership. In this blog post, we’ll discuss the challenges millennials might encounter, provide practical tips to overcome them, and highlight the long-term benefits of homeownership as a sound investment.

Saving for a Down Payment: Start early and create a budget that allows for consistent savings. Consider cutting back on unnecessary expenses and explore down payment assistance programs or grants that can help bridge the financial gap.

Managing Student Loan Debt: Prioritize paying off high-interest debts and explore loan forgiveness programs or income-driven repayment plans. By improving your debt-to-income ratio, you’ll enhance your chances of qualifying for a mortgage.

Assessing Affordability: Determine how much home you can afford by analyzing your income, expenses, and lifestyle. Consider using online calculators to estimate monthly mortgage payments and factor in additional costs like property taxes, insurance, and maintenance.

Exploring Alternative Housing Options: Don’t be afraid to think outside the box. Consider starter homes, fixer-uppers, or townhouses as potential affordable options. Being open to different types of properties can widen your choices.

Get Pre-Approved for a Mortgage: Prior to house hunting, obtain a pre-approval from a lender. This demonstrates your seriousness to sellers and gives you a competitive edge.

Working with a Knowledgeable Realtor: Collaborate with a real estate agent who specializes in working with millennial homebuyers. They can provide valuable insights, guide you through the process, and help you make informed decisions.

Utilizing Online Tools: Make the most of the real estate website and app available on our platform, which provides comprehensive property listings, up-to-date market trends, and user-friendly mortgage calculators. By leveraging these tools, you can conduct thorough research and efficiently narrow down your options. Our platform empowers you to explore a wide range of properties, stay informed about market dynamics, and make well-informed decisions throughout your home-buying journey.

Neighborhood Research: Dig deep into the neighborhoods you’re considering. Look for amenities, schools, safety ratings, and proximity to your workplace or desired locations. Online forums and social media groups can provide valuable insights from current residents.

Building Equity and Wealth: Homeownership offers the opportunity to build equity over time. Rather than paying rent, your mortgage payments contribute to long-term wealth creation.

Tax Benefits: Familiarize yourself with tax advantages associated with homeownership, such as deductions for mortgage interest and property taxes. Consult a tax professional for personalized advice.

While the housing market may present challenges for millennials, it’s important to approach homeownership with careful planning and determination. By overcoming financial hurdles, adapting to the competitive market, embracing technology, and considering the long-term benefits, millennials can achieve their dream of owning a home. Remember, homeownership is not just a place to live but a pathway to financial stability and a valuable investment for the future. With the right guidance and informed decisions, millennials can navigate the housing market with confidence and turn their dreams into reality.

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

You’re probably feeling the impact of high inflation every day as prices have gone up on groceries, gas, and more. If you’re a renter, you’re likely experiencing it a lot as your rent continues to rise. Between all of those elevated costs and uncertainty about a potential recession, you may be wondering if it still makes sense to buy a home today. The short answer is – it does. Here’s why.

Homeownership actually shields you from the rising costs inflation brings.

Freddie Mac explains how:

“Not only will buying today help you begin to build equity, a fixed-rate mortgage can stabilize your monthly housing costs for the long-term even while other life expenses continue to rise – as has been the case the past few years.”

Unlike rents, which tend to rise with time, a fixed-rate mortgage payment is predictable over the life of the mortgage (typically 15 to 30 years). And, when the cost of most everything else is rising, keeping your housing payment stable is especially important.

The alternative to homeownership is renting – and rents tend to move alongside inflation. That means as inflation goes up, your monthly rent payments tend to go up, too (see graph below):

A fixed-rate mortgage allows you to protect yourself from future rent hikes. With inflation still high, when your rental agreement comes up for renewal, your property manager may decide to increase your payments to offset the impact of inflation. Maybe that’s why, according to a recent survey, 73% of property managers plan to raise rents over the next two years.

Having your largest monthly expense remain stable in a time of economic uncertainty is a major perk of homeownership. If you continue to rent, you don’t have that same benefit and aren’t as protected from rising costs.

A stable housing payment is especially important in times of high inflation. Connect with me so you can learn more and start your journey to homeownership today.

Article Source: www.keepingcurrentmatters.com

As the summer heat approaches, it’s essential to find ways to stay cool without breaking the bank. By implementing these simple yet effective energy-saving tips, you can keep both the temperature and your budget well within the comfort zone. From optimizing your air conditioning to making small adjustments in your daily routines, these tips will help you beat the heat while reducing your energy consumption. Embrace these strategies and enjoy a refreshing summer while keeping your energy bill in check.

To ensure your air conditioner operates efficiently throughout the summer, regular maintenance is key. While professional servicing is recommended, you can still perform basic checks yourself. Vacuum air vents regularly to remove dust buildup, ensure proper airflow by keeping furniture away from vents, and avoid placing heat-generating appliances near your thermostat. These simple steps will help your A/C cool your space effectively while minimizing energy waste.

Maintaining a clean air filter is crucial for the smooth operation of your air conditioning system. Clogged filters hinder airflow and reduce the A/C’s ability to absorb heat efficiently. Make it a habit to clean or replace your air filter every month or two, and increase the frequency if you have pets or live in a dusty environment. This simple task can lower your energy usage by up to 15%.

Swap out outdated incandescent bulbs with energy-efficient LED lights. Unlike incandescent bulbs, which waste energy as heat, LEDs convert a significantly higher percentage of electricity into light. LED lights are not only more environmentally friendly but also last longer, consume 75% less energy, and emit less heat. Though they may cost slightly more upfront, their long-term energy savings make them a worthwhile investment.

Set your thermostat to a comfortable but energy-efficient temperature, ideally around 78°F or higher. Each degree you raise the setting can save you 6 to 8 percent on cooling costs. When no one is home, adjust the temperature higher to conserve energy and lower it only when necessary. Consider upgrading to a smart thermostat that adapts to your schedule and automatically adjusts temperatures for optimal efficiency. Additionally, explore potential rebates and discounts offered by your energy provider for installing a smart thermostat.

Utilize fans strategically to enhance the cooling effect of your air conditioning. Ceiling fans, for example, create a wind chill effect that allows you to set your thermostat a few degrees higher without sacrificing comfort. Remember to turn off fans when leaving the room to avoid unnecessary energy consumption.

To prevent your home from turning into a greenhouse, close your blinds or drapes during the daytime, particularly on south- and west-facing windows. This simple step will minimize the sun’s heat from entering your home and keep your space cooler naturally. Leave north-facing windows uncovered to let in natural light without significant heat gain.

In hot and humid climates, a dehumidifier can be a valuable companion to your air conditioning system. By reducing humidity levels, a dehumidifier helps your A/C work more efficiently and saves energy. Excessive humidity forces your A/C to cool and dehumidify simultaneously, leading to increased energy consumption and potential strain on the system. An energy-efficient dehumidifier alleviates this strain, promoting both comfort and cost savings.

Avoid using your oven during the hot summer months, as it adds unwanted heat to your home. Opt for alternative cooking methods such as microwaving or slow cooking, which generate less heat. Embrace the opportunity to enjoy outdoor grilling, keeping the heat outside while relishing delicious meals.

Cut down on hot water usage by washing clothes and dishes with cold water whenever possible. Washing full loads conserves water and reduces the frequency of running appliances. Additionally, consider air-drying your clothes instead of using the dryer, as this saves energy and extends the lifespan of your garments. Lowering the temperature on your water heater also contributes to energy savings while maintaining comfort.

Even when switched off, electronics consume a small amount of energy and generate heat when plugged in. Unplug devices that aren’t in use to reduce unnecessary heat buildup and save energy. Cumulatively, these small adjustments can make a noticeable difference in your overall energy consumption.

Proper insulation is essential not only during winter but also in the summer months. Air leaks can allow warm air to enter your home and cool air to escape, forcing your A/C to work harder. Seal cracks and gaps around windows, doors, and other openings with caulk and weather-stripping. Ensure your attic and basement are properly insulated, as these areas are prone to air leaks. By keeping your home tightly sealed, you can enjoy energy savings year-round.

Implementing these energy-saving tips will not only help you beat the summer heat but also reduce your energy bill. From optimizing your air conditioning to adopting smart habits in your daily routines, small changes can have a significant impact. Embrace energy efficiency and enjoy a refreshing summer while keeping both your comfort and budget in mind. Start implementing these tips today and continue saving energy throughout the year.

If you’re looking to buy a house, you may find today’s limited supply of homes available for sale challenging. When housing inventory is as low as it is right now, it can feel like a bit of an uphill battle to find the perfect home for you because there just isn’t that much to choose from. If you need to open up your pool of options, it may be time to consider a newly built home.

According to the latest data from the U.S. Census, there’s positive news when it comes to new home construction. When you look at the first three months of this year, you’ll find:

• More new homes were completed and are ready to sell. This gives you more move-in-ready options for your search.

• Builders broke ground and started construction on more single-family homes. This means there are more homes intended for one household in the beginning stages of construction, allowing you the opportunity to customize one to your liking.

• The number of permits for building new single-family homes ticked up. This shows builders are ramping up to start on even more home construction soon.

And, while this is all good news for broadening your options for your home search, there are other perks that come with considering a newly built home.

When you buy a new home under construction, you can tailor it to your unique needs and taste. Bankrate says:

“Building means customizing. . . . instead of wishing your home had a certain kind of flooring, a sunroom or some other special amenity, you’ll be able to tailor the property to your exact needs.”

Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

And, because everything is new, you’ll likely find there are fewer maintenance and repair needs up front. As Realtor.com explains:

“. . . if something does go wrong with your new home, not only are there likely some manufacturer warranties in place, but many builders also include additional home warranties . . .”

Lastly, building a home gives you the opportunity to incorporate more energy-efficient options that can help lower your costs over time – which can feel especially important when inflation’s raising many of the costs around you.

In today’s competitive real estate market, finding your dream home can be a daunting task. However, exploring the option of newly built homes can provide you with the flexibility to customize your living space while taking advantage of modern amenities and energy-efficient features. Working with me can help you navigate the process of buying a newly built home and find the perfect fit for your lifestyle and budget. So, if you’re struggling to find your ideal home, consider a newly built property and take the first step towards your dream home today.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

Wondering if you should continue renting or if you should buy a home this year? If so, consider this. Rental affordability is still a challenge and has been for years. That’s because, historically, rents trend up over time. Data from the Census shows rents have been climbing pretty steadily since 1988.

And, data from the latest rental report from Realtor.com shows rents continue to grow today, even though it’s at a slower pace than we saw at the height of the pandemic:

“In March 2023, the U.S. rental market experienced single-digit growth for the eighth month in a row . . . The median asking rent was $1,732, up by $15 from last month and down by $32 from the peak but is still $354 (25.7%) higher than the same time in 2019 (pre-pandemic).”

With rents much higher now than they were in more normal, pre-pandemic years, owning your home may be a better option, especially if the long-term trend of rents increasing each year continues. In contrast, homeowners with a fixed-rate mortgage can lock in a monthly mortgage payment for the duration of their loan (typically 15-30 years).

The graph below uses national data on the median rental payment from Realtor.com and median mortgage payment from the National Association of Realtors (NAR) to compare the two options. As the graph shows, depending on how much space you need, it’s typically more affordable to own than to rent if you need two or more bedrooms:

So, if you’re looking to live somewhere where you have two or more bedrooms to accommodate your household, give you more breathing room to spread out your belongings, or dedicate the extra space to practice your hobbies, it might make sense to consider homeownership.

In addition to shielding you from rising rents and being more affordable when you need more space, owning your home also allows you to start building your own equity, which in turn grows your net worth.

And, as home values typically rise over time and you pay off your mortgage, you build equity. That equity can set you up for success later on because you can use it to help fuel a move to an even bigger space down the line. That’s why, according to Zonda, the top reason millennial homeowners bought their home over the past year was to build their own equity instead of someone else’s.

Making the decision to buy a home versus continuing to rent can be a complex process, but with the help of a trusted real estate agent, you can explore your options and make an informed decision. As rents continue to rise, now may be the perfect time to pursue your dream of homeownership and start building equity in your own property. Don’t hesitate to reach out to today and see how they can help you navigate the home buying process.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

As the housing market continues to change, you may be wondering where it’ll go from here. One factor you’re probably thinking about is home prices, which have come down a bit since they peaked last June. And you’ve likely heard something in the news or on social media about a price crash on the horizon. As a result, you may be holding off on buying a home until prices drop significantly. But that’s not the best strategy.

A recent survey from Zonda shows 53% of millennials are still renting right now because they’re waiting for home prices to come down. But here’s the thing: the most recent data shows that home prices appear to have bottomed out and are now on the rise again. Selma Hepp, Chief Economist at CoreLogic, reports:

“U.S. home prices rose by 0.8% in February . . . indicating that prices in most markets have already bottomed out.”

And the latest data from Black Knight shows the same shift. The graph below compares home price trends in November to those in February:

So, should you keep waiting to buy a home until prices come down? If you factor in what the experts are saying, you probably shouldn’t. The data shows prices are increasing in much of the country, not decreasing. And the latest data from the Home Price Expectation Survey indicates that experts project home prices will rise steadily and return to more normal levels of appreciation after 2023. The best way to understand what home values are doing in your area is to work with a local real estate professional who can give you the latest insights and expert advice.

If you’re postponing your home-buying plans in hopes of prices coming down, it may be time to reconsider. Real estate markets are cyclical, and waiting may result in missed opportunities for potential appreciation. Additionally, factors such as interest rates and limited inventory can impact affordability and competitiveness in the market. I can help you stay informed about what’s happening in your local housing market and make informed decisions about when to buy. Don’t miss out on your dream home – contact me today to understand the current dynamics of the market.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

There have been a lot of shifts in the housing market recently. Mortgage rates rose dramatically last year, impacting many people’s ability to buy a home. And after several years of rapid price appreciation, home prices finally peaked last summer. These changes led to a rise in headlines saying prices would end up crashing.

Even though we’re no longer seeing the buyer frenzy that drove home values up during the pandemic, prices have been relatively flat at the national level. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), doesn’t expect that to change:

“[H]ome prices will be steady in most parts of the country with a minor change in the national median home price.”

You might think sellers would have to lower prices to attract buyers in today’s market, and that’s part of why some may have been waiting for prices to come crashing down. But there’s another factor at play – low inventory. And according to Yun, that’s limiting just how low prices will go:

“We simply don’t have enough inventory. Will some markets see a price decline? Yes. [But] with the supply not being there, the repeat of a 30 percent price decline is highly, highly unlikely.”

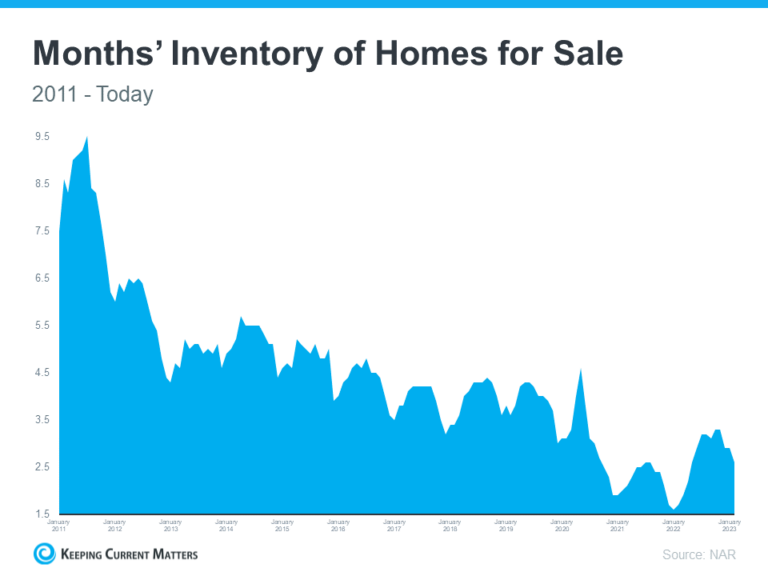

As you can see in the graph below, we’ve been at or near record-low inventory levels for a few years now.

That lack of available homes on the market is putting upward pressure on prices. Bankrate puts it like this:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

If more homes don’t come to the market, a lack of supply will keep prices from crashing, and, according to industry expert Rick Sharga, inventory isn’t likely to rise significantly this year:

“I believe that we’re likely to see low inventory continue to vex the housing market throughout 2023.”

Sellers are under no pressure to move since they have plenty of equity right now. That equity acts as a cushion for homeowners, lowering the chances of distressed sales like foreclosures and short sales. And with many homeowners locked into low mortgage rates, that equity cushion isn’t going anywhere soon.

With so few homes available for sale today, it’s important to work with a trusted real estate agent who understands your local area and can navigate the current market volatility.

Despite low buyer demand, prices are not crashing in the current real estate market. The main reason for this is the shortage of homes for sale. If you’re considering moving this spring, it’s essential to work with a trusted real estate agent who can help you navigate the competitive market and increase your chances of finding a suitable home. Don’t miss out on the opportunity to partner with me and make informed decisions in today’s real estate market.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

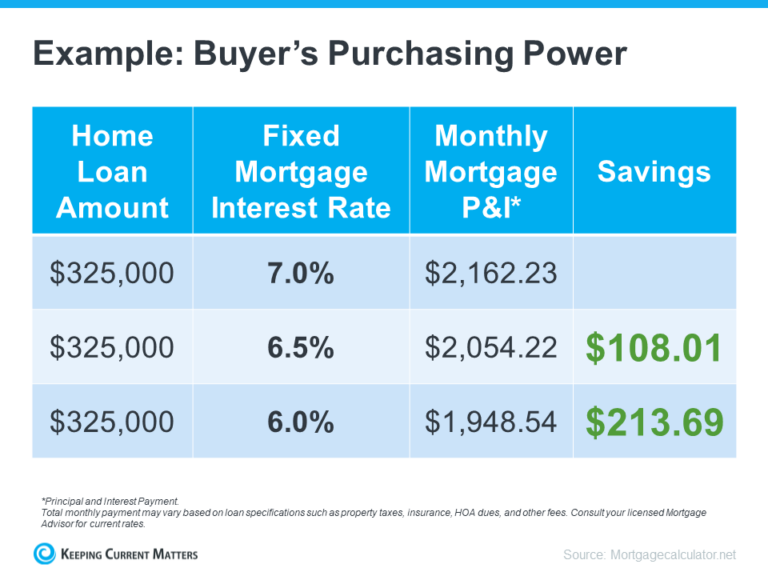

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power.

The chart below helps show the general relationship between mortgage rates and a typical monthly mortgage payment:

Even a 0.5% change can have a big impact on your monthly payment. And since rates have been moving between 6% and 7% for a while now, you can see how it impacts your purchasing power as rates go down.

You may be tempted to put your homebuying plans on hold in hopes that rates will fall. But that can be risky. No one knows for sure where rates will go from here, and trying to time them for your benefit is tough. Lisa Sturtevant, Housing Economist at Bright MLS, explains:

“It is typically a fool’s errand for a homebuyer to try to time rates in this market . . . But volatility in mortgage rates right now can have a real impact on buyers’ monthly payments.”

That’s why it’s critical to lean on your expert real estate advisors to explore your mortgage options, understand what impacts mortgage rates, and plan your homebuying budget around today’s volatility. They’ll also be able to offer advice tailored to your specific situation and goals, so you have what you need to make an informed decision.

There are a complex set of factors that impact mortgage interest rates, including broader economic conditions, the monetary actions of the Federal Reserve (to some extent) and inflation. However, long-term mortgage rates are directly impacted by the bond market. The rate you’re offered on a mortgage will also depend on the lender you work with, its business costs and your financial profile.

Demand for mortgages can also affect rates, pushing it higher as available capital for lending tightens. Conversely, when there’s less borrower demand—as we’re seeing now due to average interest rates hovering in the 6% to 7% range—lenders might consider offering more competitive rates or other incentives to attract borrowers.

It’s clear that changing mortgage rates can have a significant impact on your ability to buy a home. With rates fluctuating between 6% and 7% this year, even a slight shift of 1% or 0.5% can make a big difference in your purchasing power. That’s why it’s important to work with a trusted real estate agent and lender to develop a strong plan when considering a move. By doing so, you can be confident in your ability to navigate the mortgage market and find the home of your dreams.

Article Source: www.keepingcurrentmatters.com

Are you looking to purchase a home this spring? With the real estate market still favoring sellers, it’s important to be strategic when it comes to making an offer. Buying a home is a significant investment, and you want to ensure that you are getting the best value for your money. By following these tips, you can increase your chances of having your offer accepted and securing the home of your dreams.

Rely on an agent who can support your goals. As Bankrate notes:

“. . . select the best real estate agent for your needs. They will be a critical part of your home buying process.”

Agents are local market experts. They know what’s worked for other buyers in your area and what sellers may be looking for in an offer. It may seem simple, but catering to what a seller needs can help your offer stand out.

“Understand your current budget … what are your expenses, how’s your spending, would you need to make changes?”

The best way to understand your numbers is to work with a lender so you can get pre-approved for a loan. It helps you be more financially confident, and it shows sellers you’re serious. That can give you a competitive edge.

Today’s market isn’t moving at the record pace it did during the pandemic. That means you may have a bit more time to think before you need to make an offer. According to Danielle Hale, Chief Economist at realtor.com:

“In general, you likely have more time to make an offer, although that’s certainly not a guarantee. If you’re on the fence about a home or its asking price doesn’t quite fit your budget, you might want to keep an eye on it, and if it doesn’t sell right away, you may have some room to negotiate with the seller.”

While it’s still important to stay on top of the market and be prepared to move quickly, there can be more flexibility today. Lean on the advice of your agent as you explore the options in your market.

During the pandemic, some buyers skipped home inspections or didn’t ask for concessions from the seller in order to submit the winning bid on a home. Fortunately, today’s market is different, and you may have more negotiating power than before. When putting together an offer, your trusted real estate advisor will help you think through what levers to pull.

When it comes to making an offer on a home, it’s crucial to be strategic and well-informed. By working with a trusted real estate advisor, you can gain valuable insights into the local market, the home’s value, and the seller’s situation. I can help you come up with a competitive offer that reflects the home’s true value while also keeping your budget in mind. With my expertise and guidance, you can increase your chances of having your offer accepted and securing your dream home. So, when you’re ready to make your move, be sure to connect with me to help you make your best offer.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

Please fill out the form below and we will be contacting you shortly

with information about your home.