Chances are at some point in your life you’ve heard the phrase, home is where the heart is. There’s a reason that’s said so often. Becoming a homeowner is emotional.

So, if you’re trying to decide if you want to keep on renting or if you’re ready to buy a home this year, here’s why it’s so easy to fall in love with homeownership.

Your house should be a space that’s uniquely you. And, if you’re a renter, that can be hard to achieve. When you rent, the paint colors are usually the standard shade of white, you don’t have much control over the upgrades, and you’ve got to be careful how many holes you put in the walls. But when you’re a homeowner, you have a lot more freedom. As the National Association of Realtors (NAR) says:

“The home is yours. You can decorate any way you want and choose the types of upgrades and new amenities that appeal to your lifestyle.”

Whether you want to paint the walls a cheery bright color or go for a dark moody tone, you can match your interior to your vibe. Imagine how it would feel to come home at the end of the day and walk into a space that feels like you.

One of the hardest things about renting is the uncertainty of what happens at the end of your lease. Does your payment go up so much that you have to move? What if your landlord decides to sell the property? It’s like you’re always waiting for the other shoe to drop. Jeff Ostrowski, a business journalist covering real estate and the economy, explains how homeownership can give you more peace of mind in a Money Geek article:

“Homeownership means you are the boss and have the biggest say in your lifestyle and family decisions. Suppose your kids are in public school and you don’t want to risk having them change schools because your landlord doesn’t renew your lease. Owning a home would remove much of the risk of having to move.”

You may also find you feel much more at home in the community once you own a house. That’s because, when you buy a home, you’re staking a claim and saying, I’m a part of this community. You’ll have neighbors, block parties, and more. And that’ll give you the feeling of being a part of something bigger. As the International Housing Association explains:

“. . . homeowning households are more socially involved in community affairs than their renting counterparts. This is due to both the fact that homeowners expect to remain in the community for a longer period of time and that homeowners have an ownership stake in the neighborhood.”

Becoming a homeowner is a journey – and it may have been a long road to get to the point where you’re ready to take the plunge. If you’re seriously considering leaving behind your rental and making this commitment, you should know the emotions that come with this owning a home are powerful. You’ll be able to walk up to your front door every day and have that sense of accomplishment welcome you home.

A home is a place that reflects who you are, a safe space for the ones you love the most, and a reflection of all you’ve accomplished. Connect with me if you’re ready to break up with your rental and buy a home.

Article Source: www.keepingcurrentmatters.com

Have you ever heard the term “Silver Tsunami” and wondered what it’s all about? If so, that might be because there’s been lot of talk about it online recently. Let’s dive into what it is and why it won’t drastically impact the housing market.

A recent article from HousingWire calls it:

“. . . a colloquialism referring to aging Americans changing their housing arrangements to accommodate aging . . .”

The thought is that as baby boomers grow older, a significant number will start downsizing their homes. Considering how large that generation is, if these moves happened in a big wave, it would affect the housing market by causing a significant uptick in the number of larger homes for sale. That influx of homes coming onto the market would impact the balance of supply and demand and more.

The concept makes sense in theory, but will it happen? And if so, when?

Experts say, so far, a silver tsunami hasn’t happened – and it probably won’t anytime soon. According to that same article from HousingWire:

“. . . the silver tsunami’s transformative potential for the U.S. housing market has not yet materialized in any meaningful way, and few expect it to anytime soon.”

Here’s just one reason why. Many baby boomers don’t want to move. Data from the AARP shows over half of the surveyed adults ages 65 and up plan to stay put and age in place in their current home rather than move (see chart below):

Clearly, not every baby boomer is planning to sell or move – and even those who do won’t do it all at once. Instead, it will be more gradual, happening slowly over time. As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

If you’re worried about a Silver Tsunami shaking up the housing market, don’t be. Any impact from baby boomers moving will be gradual over many years. Fleming sums it up best:

“Demographic trends, they don’t tsunami. They trickle.”

Connect with me to discuss how these trends may affect your specific situation and explore strategies for a stable future.

Article Source: www.keepingcurrentmatters.com

In the dynamic and competitive real estate market of 2024, securing your dream home at the best possible terms requires a strategic approach to negotiation. As a savvy homebuyer, understanding the intricacies of negotiation can make all the difference in turning your homeownership aspirations into reality. In this comprehensive guide, we’ll explore effective negotiation strategies tailored to the unique challenges and opportunities of the current real estate landscape.

Knowledge is power, and this holds true in real estate negotiations. Arm yourself with thorough research on the local market trends, recent property sales, and the specific neighborhood you’re interested in. Being well-informed about comparable properties and recent sales prices empowers you to negotiate from a position of strength.

Before entering negotiations, define your priorities and deal-breakers. Establishing a clear understanding of your must-haves and non-negotiables allows you to focus on what truly matters. Equally important is setting realistic limits on your budget and terms, ensuring you don’t compromise your financial stability for the sake of a deal.

Engaging a seasoned real estate agent can be a game-changer in negotiations. Realtors bring market expertise, negotiation skills, and a network of industry contacts to the table. Their experience can help you navigate complex negotiations, ensuring that your interests are protected and that you secure the best possible deal.

In a competitive market, the temptation to rush through negotiations can be strong. However, patience is a virtue, especially in real estate. Take the time to carefully evaluate each offer and counteroffer. Don’t be afraid to walk away from a deal that doesn’t align with your priorities. A patient and discerning approach will increase your chances of landing a favorable agreement.

Understanding the seller’s motivation can provide valuable insights into their willingness to negotiate. Are they in a hurry to sell due to a job relocation or financial constraints? Or are they testing the waters with their property? Tailor your negotiation strategy based on the seller’s situation to enhance your leverage.

Flexibility in negotiation doesn’t mean compromising on your priorities. Instead, it involves being open to creative solutions that meet both parties’ needs. This can include adjustments in closing dates, repairs, or other terms that contribute to a win-win scenario.

Including well-crafted contingencies in your offer provides you with an exit strategy if the negotiation doesn’t go as planned. Common contingencies include home inspections, financing, and the sale of your current property. Having these safeguards in place allows you to negotiate with confidence, knowing you have options.

Successful negotiation in the 2024 real estate market requires a combination of preparation, strategy, and adaptability. By leveraging these tips, you’ll be well-equipped to navigate negotiations with confidence, securing the best possible terms and pricing for your new home.

Ready to embark on your homebuying journey? Connect with me today to discuss your specific needs and to get personalized guidance on navigating the real estate market. Your dream home awaits – let’s make it a reality together.

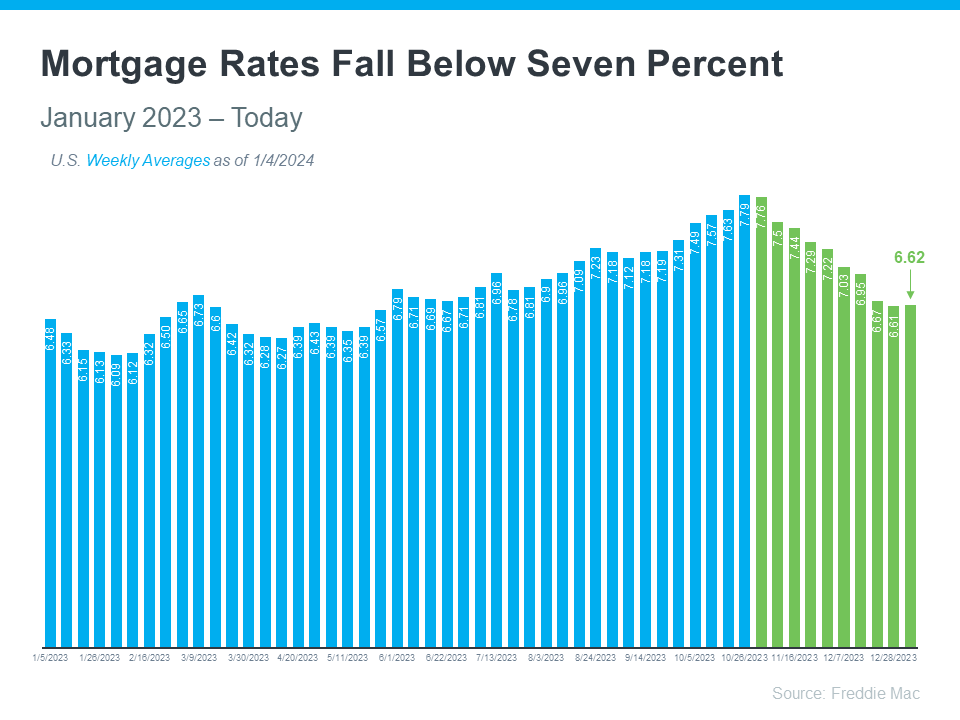

If you want to buy a home, it’s important to know how mortgage rates impact what you can afford and how much you’ll pay each month. Fortunately, rates for 30-year fixed mortgages have come down significantly since the end of October and are currently under 7%, according to Freddie Mac (see graph below):

This recent trend is great news for buyers. As a recent article from Bankrate says:

“The rate cool-off somewhat eases the housing affordability squeeze.”

And according to Edward Seiler, AVP of Housing Economics and Executive Director of the Research Institute for Housing America at the Mortgage Bankers Association (MBA):

“MBA expects that affordability conditions will continue to improve as mortgage rates decline . . .”

Here’s a bit more context on how this could help with your plans to buy a home.

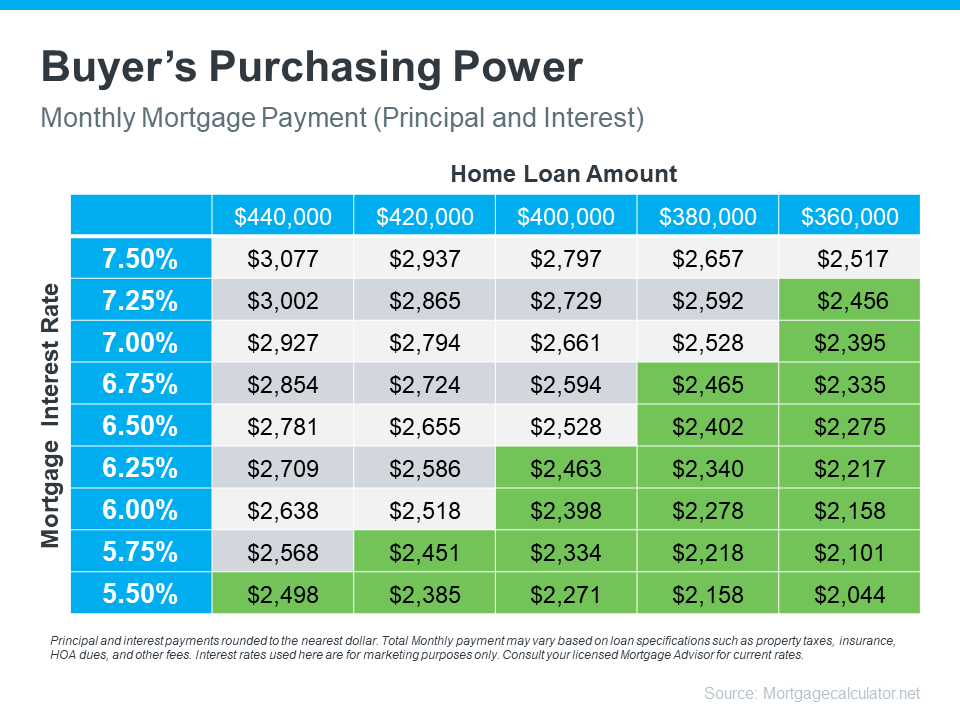

Understanding the connection between mortgage rates and your monthly home payment is crucial for your plans to become a homeowner. The chart below illustrates how your ability to afford a home changes when mortgage rates shift. Imagine your budget allows for a monthly payment between $2,400 and $2,500. The green part in the chart shows payments in that range or lower (see chart below):

As you can see, even small changes in rates can affect your budget and the loan amount you can afford.

When you’re looking to buy a home, it’s important to get guidance from a local real estate agent and a trusted lender. They can help you explore different mortgage options, understand what makes mortgage rates go up or down, and how those changes impact you.

By looking at the numbers and the latest data together, then adjusting your strategy based on today’s rates, you’ll be better prepared and ready to buy a home.

If you’re looking to buy a home, you should know the recent downward trend in mortgage rates is good news for your move. Connect with me to explore the best options in today’s market and turn your homeownership aspirations into a successful reality.

Article Source: www.keepingcurrentmatters.com

Welcome to 2024, where new beginnings and fresh opportunities await! If you’re considering embarking on the exciting journey of homeownership in Venice and North Port, Florida, this article is your compass for navigating the real estate landscape in the new year. In this exclusive guide, we present strategic resolutions tailored to the unique needs and considerations of our local market. Let’s make 2024 the year you find your dream home.

Before delving into the house-hunting adventure, it’s crucial to assess and enhance your financial fitness. Consider these resolutions to set a solid foundation:

Work closely with a financial advisor to determine a budget that aligns with your financial goals and local market trends. Factor in not only the purchase price but also closing costs, property taxes, and potential renovations.

A stellar credit score opens doors to favorable mortgage rates. Resolve to check your credit report regularly, address any discrepancies, and make strategic financial decisions to improve your score.

Venice and North Port boast a variety of neighborhoods, each with its own charm. Resolve to explore different areas, considering factors like proximity to amenities, school districts, and lifestyle preferences.

Collaborate with experienced local real estate agents who have an in-depth understanding of the market. Their insights can be invaluable in navigating the complexities and finding the best opportunities.

Create a list of non-negotiable features your dream home must have, such as the number of bedrooms, outdoor space, or specific amenities. This will help streamline your search and focus on properties that align with your vision.

Venice and North Port are dynamic communities. Anticipate future needs and growth, whether it’s a growing family or changing lifestyle preferences. Opt for a property that accommodates both your present and future requirements.

Don’t skimp on property inspections. Resolution to hire professionals to assess the property’s condition, ensuring there are no hidden surprises. This step is crucial for making informed decisions and negotiating repairs if needed.

Real estate transactions involve a mountain of paperwork. Resolve to carefully review all contracts, disclosures, and legal documents. If necessary, seek legal advice to ensure you fully comprehend the terms and conditions of the transaction.

Make your new house a home by personalizing it. Whether it’s a fresh coat of paint, landscaping, or interior decor, adding your touch enhances the living experience.

Venice and North Port are communities with a strong sense of camaraderie. Resolve to engage with local events, join community groups, and become an active participant in the vibrant local culture.

As you embark on your journey toward homeownership in 2024, remember that each resolution brings you closer to realizing your dream. By aligning your financial goals, understanding the local market, defining your vision, and navigating the buying process diligently, you’ll be well on your way to making this year the one where you call Venice or North Port your home. Happy house hunting!

As the new year approaches, the idea of buying a home might be on your mind. It’s an exciting goal to set, and it’s never too early to start laying the groundwork. One crucial step to prepare for homeownership is building a solid credit score.

Lenders review your credit to assess your ability to make payments on time, pay back debts, and more. It’s also a factor that helps determine your mortgage rate. An article from CNBC explains:

“When it comes to mortgages, a higher credit score can save you thousands of dollars in the long run. This is because your credit score directly impacts your mortgage rate, which determines the amount of interest you’ll pay over the life of the loan.”

This means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability, especially today.

According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. An article from Business Insider explains generally how your FICO score range can make an impact:

“. . . you don’t need a perfect credit score to buy a house. . . . Aiming to get your credit score in the ‘Good’ range (670 to 739) would be a great start towards qualifying for a mortgage. But if you’re wanting to qualify for the lowest rates, try to get your score within the ‘Very Good’ range (740 to 799).”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate. As FICO says:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experian highlights some things you may want to focus on:

• Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

• Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

• Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

A lender will help you navigate the process from start to finish, from assessing which range your score falls in to telling you more about the specifics for each loan type.

As you set your sights on buying a home in the upcoming year, a focus on boosting your credit score could help you get a better mortgage rate when the time comes. Let’s connect, and I will seamlessly facilitate your connection with my trusted lender, ensuring you receive expert assistance throughout the home buying process. Your dream home awaits – let’s make it a reality together.

Article Source: www.keepingcurrentmatters.com

Considering a new home? Cash transactions in real estate have a timeless allure, often hailed with the phrase, “cash is king.” But before you embrace this age-old wisdom and embark on the journey of buying a house with cash, there are crucial factors to weigh. Let’s explore the considerations and steps involved in making this significant financial decision.

If you’re in the market for a new home, you’ve likely heard the age-old saying that “cash is king.” But is it really? Should you consider buying a house with cash? Before you dive headfirst into this financial decision, it’s crucial to consider a few key factors.

Before deciding to purchase a house with cash, take a close look at your financial situation. Evaluate your savings, investments, and overall liquidity. Buying a house with cash can be a wise move if it won’t significantly deplete your savings or hinder your ability to cover unforeseen expenses.

Consider the opportunity cost of using your cash to buy a house outright. Could that money potentially generate higher returns if invested elsewhere? It’s essential to weigh the benefits of owning a home outright against the potential returns from other investment opportunities.

Keep an eye on the real estate market. In a competitive market, a cash offer can be more attractive to sellers, potentially giving you an upper hand in negotiations. However, in a buyer’s market, you might have more negotiating power when financing the purchase.

If you’ve decided that buying a house with cash is the right move for you, the process is relatively straightforward. Here’s a brief guide on how to navigate the cash-buying process:

Before making an offer, you’ll need to provide proof of funds to the seller. This can be a bank statement or a letter from your financial institution confirming your ability to cover the purchase price.

With a cash offer, you may have more room to negotiate on price. Sellers often prefer cash deals due to the quicker and more straightforward transaction process.

Even if you’re paying in cash, due diligence is crucial. Hire a qualified home inspector to identify any potential issues with the property, ensuring you make an informed decision.

Regardless of how you choose to finance your home purchase, due diligence is a critical step. When paying cash, it’s essential to:

Dig into the property’s history, including any previous sales, title issues, or liens. Understanding the property’s background helps you avoid potential headaches down the road.

Ensure that all legal aspects of the transaction are in order. This includes zoning regulations, property taxes, and any restrictions that may affect your use of the property.

A comprehensive home inspection is essential, even in a cash transaction. Identify any issues that may impact the property’s value or your quality of life.

Let’s break down the advantages and disadvantages of paying cash for a house:

• Faster Closing: Cash transactions typically close faster than financed deals.

• Negotiating Power: Sellers often prefer cash offers and may be more willing to negotiate on price.

• No Interest Payments: Without a mortgage, you’ll avoid paying interest over the life of the loan.

• Opportunity Cost: Using cash may limit your ability to invest in other opportunities.

• Reduced Liquidity: Tying up a significant amount of cash in a home could limit your liquidity.

• Missed Tax Deductions: You won’t benefit from mortgage interest tax deductions if you pay with cash.

Buying a house with cash can be a strategic move, but it’s essential to carefully weigh the pros and cons. Consider your financial situation, the current real estate market conditions, and the long-term implications of tying up your cash in a property. Whether you choose to pay with cash or opt for financing, thorough due diligence is the key to making a wise and informed decision.

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

If you’re thinking about buying or selling a home, you might have heard that it’s tough right now because mortgage rates are higher than they’ve been over the past few years, and home prices are rising. That much is true. Take a look at the graph below. It breaks down how the current affordability situation stacks up to recent years.

The National Association of Realtors (NAR) explains how to read the values on the graph:

“To interpret the indices, a value of 100 means that a family with the median income has exactly enough income to qualify for a mortgage on a median-priced home.”

The black dotted line represents that 100 value on the index. Essentially, the higher the bar, the more affordable homes are. As you can see, the orange bar for today shows higher mortgage rates and home prices have created a clear challenge. But, while affordability is definitely tighter right now, that doesn’t mean the housing market is at a standstill.

According to NAR, based on the pace of sales right now, just under 4 million homes will sell this year. With some simple math, let’s break down what that really means for you:

So, on average, over 10,000 homes sell each day in this country. Whether you’re a buyer or a seller, this goes to show there are still ways to make your move possible, even at a time when affordability is tight.

You may be wondering how other homebuyers and sellers are making this happen now. One of the biggest game-changers in today’s market is working with a trusted local real estate agent. Great agents are helping other people just like you navigate today’s market and the current affordability situation, and their insight is invaluable right now.

True professionals will be able to offer advice tailored to your specific wants, needs, budget, and more. Not to mention, they’ll also be able to draw on their experience of what’s working for other buyers and sellers right now. This could mean broadening your search, if needed, to include other housing types like condos, townhouses, or neighborhoods a bit further out to help offset some of the affordability challenges today.

You might think there aren’t many people buying or selling homes right now since affordability is tighter than it’s been in quite some time, but that’s not the case. It’s true that buying a home has become more expensive over the past couple of years, but people are still moving.

If you’re hoping to buy or sell a home today, know that other people are still making their goals a reality – and that’s happening in large part because of the help and advice of skilled real estate agents. Let’s make it happen together. Reach out and connect with a local real estate agent who’s ready to turn your dreams into keys.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

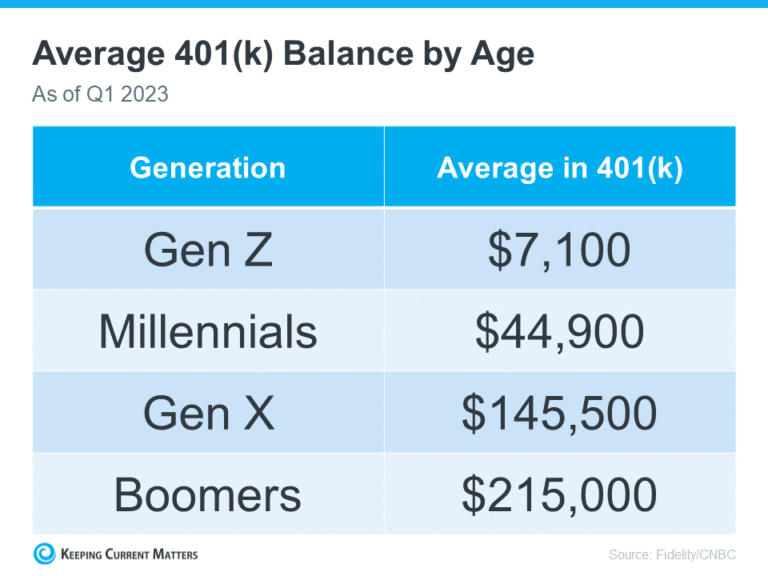

Are you dreaming of buying your own home and wondering about how you’ll save for a down payment? You’re not alone. Some people think about tapping into their 401(k) savings to make it happen. But before you decide to dip into your retirement to buy a home, be sure to consider all possible alternatives and talk with a financial expert. Here’s why.

The data shows many Americans have saved a considerable amount for retirement (see chart below):

It can be really tempting when you have a lot of money saved up in your 401(k) and you see your dream home on the horizon. But remember, dipping into your retirement savings for a home could cost you a penalty and affect your finances later on. That’s why it’s important to explore all your options when it comes to saving for a down payment and buying a home. As Experian says:

“It’s possible to use funds from your 401(k) to buy a house, but whether you should depends on several factors, including taxes and penalties, how much you’ve already saved and your unique financial circumstances.”

Using your 401(k) is one way to finance a home, but it’s not the only option. Before you decide, consider a couple of other methods, courtesy of Experian:

No matter what route you take to purchase a home, be sure to talk with a financial expert before you do anything. Working with a team of experts to develop a concrete plan prior to starting your journey to homeownership is the key to success. Kelly Palmer, Founder of The Wealthy Parent, says:

“I have seen parents pausing contributions to their retirement plans in favor of affording a larger home often with the hope they can refinance in the future… As long as there is a tangible plan in place to get back to saving for their retirement goals, I encourage families to consider all their options.”

If you’re contemplating using your 401(k) retirement savings for a home down payment, it’s essential to carefully weigh all your options. I’m here to assist you, and I can connect you with my trusted financial professional to guide you before you make any decisions.

Article Source: www.keepingcurrentmatters.com

I can help you find a strong buyer strategy that fits your goals. If you consider buying a property in the next 1-2 years, you need to download our free buyer guide!

Get informed with our buyer guide to understanding the best buyer strategies to get started.

Please fill out the form below and we will be contacting you shortly

with information about your home.