Whether you’ve just retired or you’re thinking about retirement, you may be considering your options and trying to picture a whole new stage of your life. And you’re not alone. Research from the Retirement Industry Trust Association (RITA) shows 10,000 Baby Boomers reach the typical retirement age (65) every day, and only 47% of the people in that generation have already retired.

If this sounds like you, one thing worth considering is whether or not your current home will suit your new lifestyle. If your home doesn’t have the features or benefits you’re looking for, the good news is, you may be in a better position to move than you realize.

That’s because, if you already own a home, you’ve likely built-up significant equity, and that can help you fuel your next move. According to the National Association of Realtors (NAR):

“A homeowner who purchased a typical home five years ago would have gained $125,300 from just price appreciation alone.”

In fact, over the last twelve months, CoreLogic reports the average homeowner in the United States gained roughly $64,000 in equity due to home price appreciation.

You can use your equity to help you achieve your homeownership goals. Whether you want to downsize, move closer to loved ones, or buy a home in a dream destination, your equity can help get you there. It may be some (if not all) of what you’d need as your down payment on a home that better fits your changing needs.

To find out how much equity to have in your home, reach out to me today.

Retirement is a big step and so is buying or selling a home. As you move into this new phase of life, a trusted real estate advisor can guide you through the process as you sell your current home and give you expert advice as you buy one that’ll better suit your needs.

Article Source: www.keepingcurrentmatters.com

It’s so easy nowadays to just go online and sift through properties that meet your criteria and price point, but most people don’t figure in the extra costs that come into play when purchasing real estate. If you’re a first time home buyer, you may not be familiar with the extra expenses that are involved with buying a home, and first time buyers aren’t alone. Even real estate veterans need to be updated or get a refresher course now and then.

The primary costs of house ownership are divided into two categories: one-time costs and ongoing costs. Down payments, closing charges, escrow prepaids, and mortgage points paid to a lender to get a reduced interest rate are examples of one-time costs. Your monthly mortgage payment, property taxes, homeowners insurance, utilities, and maintenance charges are all ongoing costs.

Here are 10 potential one-time and ongoing costs of owning a home that you should be aware of before you begin looking.

We’ll begin with the most obvious cost. When purchasing your first home, you will most likely need to secure a loan from a mortgage provider. So, unless you buy your house in cash, you’ll have to make a monthly mortgage payment. A portion of that payment will be applied to your principal debt, while the remainder will be utilized to pay insurance to your lender.

You must pay property taxes on your house every year. Property taxes might vary greatly depending on where you live. If you have a mortgage, you will usually pay your property taxes in monthly installments to your lender. The lender will place the cash in escrow and pay your whole property tax bill ahead of time.

If you have a mortgage on your home, you will almost certainly be obliged to keep a homeowners insurance policy. Even if you buy your house entirely, it’s a good idea to have insurance. Homeowners insurance can protect you in the case of a disaster, such as a fire. This is another expenditure that is often paid on a monthly basis. In reality, the frequently necessary combination of principle, interest, taxes, and insurance is commonly referred to as PITI.

It is important to note that some occurrences, such as floods, are not covered by standard homeowners’ policy. If you live in a flood-prone location, your lender may need you to purchase separate flood insurance, and in some hurricane-prone areas, windstorm insurance is also required. If you want to know what to expect in your local real estate market, talk to a local insurance agent about the needed (and optional) forms of homes insurance.

If you put less than 20% down on a home, your lender will almost certainly need you to purchase private mortgage insurance, which will be added to your monthly mortgage payment. FHA loans need their own mortgage insurance, although conventional and other mortgage borrowers can get private mortgage insurance, or PMI. This cost varies greatly based on the type of mortgage and the amount of money you put down. You can request to cancel your mortgage insurance after you pay down the loan to a loan-to-value (LTV) ratio of 80%.

Property taxes, homeowners insurance, and mortgage insurance are all often added to your mortgage payment and placed into an escrow account. Your escrow account, however, does not begin at zero; you will almost certainly be asked to make an initial deposit at closing. This will provide some reserves for your account in the event that your property taxes or insurance costs end up being greater than the lender’s initial estimate.

Closing costs are another expense that can vary greatly depending on your house, location, and a number of other factors. Closing expenses are typically 1% to 3% of the home’s purchase price, although they can be much more, particularly in low-priced homes.

Aside from the previously stated prices (points, prepaids), common closing costs include your lender’s fees for loan origination, processing, and underwriting, appraisal fees, title insurance, deed recording fees, document prep fees, and credit report fees, to name a few.

Most people who have an apartment paying monthly rent are used to paying certain utilities, particularly electricity, cable, and internet. When you purchase a home you must pay several utilities on a regular basis that you are not accustomed to. Water is frequently included in rental units, as are sewer and garbage collection costs. Be sure to budget for these when looking for a home.

If you’re moving into a neighbourhood, you’ll almost certainly be required to pay a homeowners association (or HOA) fee. These might vary greatly depending on your location and the services included by your HOA dues.

Here’s the greatest wild card cost you’ll have to budget for. Your house will require maintenance over time, and if you’ve previously rented, maintenance was most likely the duty of your landlord. Home maintenance expenses can range from basic charges such as changing air filters to substantial ones such as roof replacement.

As a general guideline, maintenance charges should be around 1% of your property’s worth every year (so $3,000 on a $300,000 home). This varies greatly from year to year and is substantially higher in older homes.

As you’ve seen above, there are many expenses associated with home ownership that can greatly impact your monthly budget. These expenses may come as a surprise to some people, especially those first-time buyers who have always dreamed of owning their own home. This article should help you realize the reality of owning a home and make sure you are on top of all of the financial commitments that come along with it.

Whether you’re a potential homebuyer, seller, or both, you probably want to know: will home prices fall this year? Let’s break down what’s happening with home prices, where experts say they’re headed, and why this matters for your homeownership goals.

“Price appreciation averaged 15% for the full year of 2021, up from the 2020 full year average of 6%.”

In other words, the pace of appreciation in 2021 far surpassed the 6% the market saw in 2020. And even that appreciation was greater than the pre-pandemic norm which was typically around 3.8%. This goes to show, 2021 was an anomaly in the housing market spurred by more buyers than homes for sale.

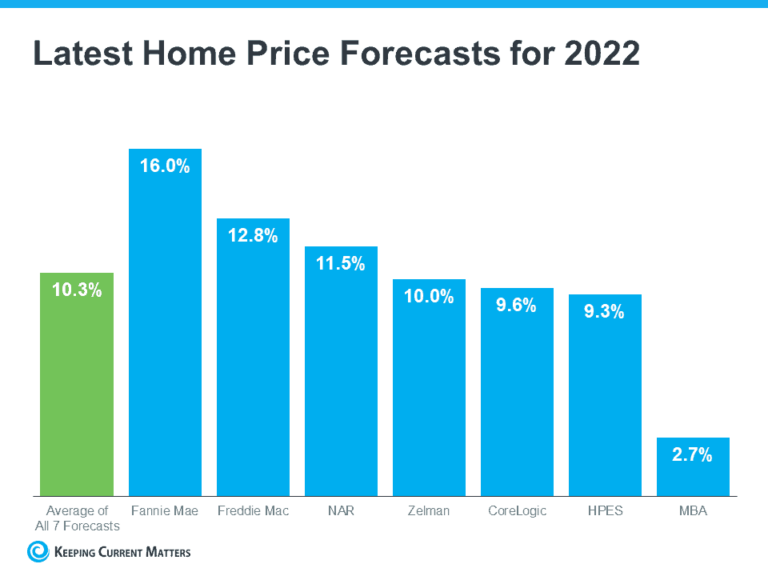

This year, home price appreciation is slowing (or decelerating) from the feverish pace the market saw over the past two years. According to the latest forecasts, experts say on average, nationwide, prices will still appreciate by roughly 10% in 2022 (see graph below):

Why do all of these experts agree prices will continue to rise? It’s simple. Even though housing supply is growing today, it’s still low overall thanks to several factors, including a long period of underbuilding homes. And experts say that’s going to help keep upward pressure on home prices this year. Additionally, since mortgage rates are higher this year than they were last year, buyer demand has slowed.

As the market undergoes this change, it’s true price appreciation this year won’t match the feverish pace in 2021. But the rapid appreciation the market saw last year wasn’t sustainable anyway.

Today, the market is beginning to move back toward pre-pandemic levels. But even the forecast for 10% home price growth in 2022 is well beyond the 3.8% that’s more typical for a normal market.

So, despite what you may have heard, experts say home prices won’t fall in most markets. They’ll just appreciate more moderately.

If you’re worried the house you’re trying to sell or the home you want to buy will decrease in value, you should know experts aren’t calling for depreciation in most markets, just deceleration. That means your home should still grow in value, just not as fast as it did last year.

Buying a house—in any market—is a highly personal decision. Because homes represent the largest single purchase most people will make in their lifetime, it’s crucial to be in a solid financial position before diving in.

Use a mortgage calculator to find out how much your monthly housing costs will be based on your down payment and interest rate.

Trying to time the market or predict what might happen next year is not the best homebuying strategy. Instead, it’s better to buy based on your budget and needs. If you find a home you love in an area you love and it also fits your budget, then chances are it might be right for you. However, if you make too many sacrifices just to get a house, you may end up with buyer’s remorse and an expensive albatross you have to offload.

If you’re thinking of making a move, you shouldn’t wait for prices to fall. Experts say nationally, prices will continue to appreciate this year, just at a more moderate pace. When you’re ready to begin the process of buying or selling, let’s connect so you have a local market expert on your side each step of the way.

If you’re planning to buy a home this season, you may be wondering how much of an offer you should make. In years past, it was common for buyers to try and determine how much less than the asking price they could offer to still get the home. The buyer and seller would then negotiate and typically agree on a revised price that was somewhere between the buyer’s bid and the home’s initial asking price.

Today’s housing market is anything but normal. According to the National Association of Realtors (NAR), the average home that’s sold today:

Homes selling quickly and receiving multiple offers shows how competitive the housing market is for buyers right now. This is because there are more buyers on the market than homes for sale. When the number of homes available can’t keep up with demand, homes often sell for more than the asking price.

Market conditions should help guide your decisions throughout the process. Today, the asking price of a home is often the floor of the negotiation rather than the ceiling. Knowing this is important when it’s time to submit an offer, but you should also use that information as you’re searching for homes too. After all, you don’t want to fall in love with a home that ultimately sells for a price higher than what you’ve budgeted for.

The Mortgage Reports has advice if you’re looking to purchase a home in a competitive market. The article encourages you to be realistic with your housing search, saying:

“The best thing to do is set your budget and expectations ahead of time so you know how much you can afford to offer — and when to walk away. This will make negotiations a lot easier.”

Of course, when you’ve found your dream home, you’ll want to do everything you can to submit your best offer up front and win a potential bidding war. Knowing the current market is key to crafting a winning offer. That’s where working with an expert real estate advisor becomes critical.

A real estate professional will draw from their experience and expert-level knowledge of today’s housing market throughout the process. They’ll also balance conditions in your area to make sure your offer stands out above the rest.

In today’s market, sellers are expecting more than just a simple negotiation; they want an offer that shows that the buyer has done their research into what similar properties in that same area are selling for. This helps them make sure they’re getting the best possible return on their investment when selling their own property.

Understanding how to approach the asking price of a home and what’s happening in today’s real estate market are critical for buyers. Let’s connect so we can work together to create a winning plan for you.

It’s true that record levels of home price appreciation have spurred significant equity gains for homeowners over the past few years. As Diana Olick, Real Estate Correspondent at CNBC, says:

“The stunning jump in home values over the course of the Covid-19 pandemic has given U.S. homeowners record amounts of housing wealth.”

That’s great for your home’s value over the last couple of years, but what if you’ve lived in your home for longer than that? You may be wondering how much equity you truly have.

The National Association of Realtors (NAR) has done a study to calculate the typical equity gains over longer spans of time. The data they compiled could be enough to motivate you to move. Just remember, to find out how much equity you have in your specific home, you’ll want to get a professional equity assessment from a trusted real estate advisor.

Let’s start by establishing how you build equity in your home. While price appreciation is clearly a factor that can help boost your equity, you also build equity over time as you pay down your home loan. NAR explains:

“Home equity gains are built up through price appreciation and by paying off the mortgage through principal payments.”

The study from NAR breaks down the typical equity gain over time (see graph below). It calculates the equity a homeowner potentially gained if they purchased the median-priced home 5, 10, or 30 years ago and still own it today.

These six-figure numbers are impressive and certainly enough to help you fuel a move into your next home, but they’re not a promised amount. Remember, your own equity gain will be different. It depends on how long you’ve been in the house, your home’s condition, any upgrades you’ve made, your area, and much more.

If you want to find out how much equity you have, partner with a trusted real estate professional for an equity assessment on your home. They can provide an expert opinion on what your house is worth today and how the equity you’ve gained over time can help you when you purchase your next home. It may be some (if not all) of what you need for your next down payment.

If you’re thinking about selling your house and making a move, home equity can be a real game-changer, especially if you’ve been in your current home for a while. If you’re ready to find out how much equity you have, let’s connect. I’m here to help you keep an eye on the market and prepare for your home purchase.

Source: www.keepingcurrentmatters.com

You may have heard that your credit score will determine whether or not you can get a mortgage and you might also know that it affects the rate and fees you pay for your loan. But did you know that it impacts everything from homeowners’ insurance rates to the price of car insurance?

Your credit score has a huge impact on your life and it could be holding you back from buying a home. While stricter lending standards could be a challenge for some, many buyers may be surprised by the options that are still available for borrowers with lower credit scores.

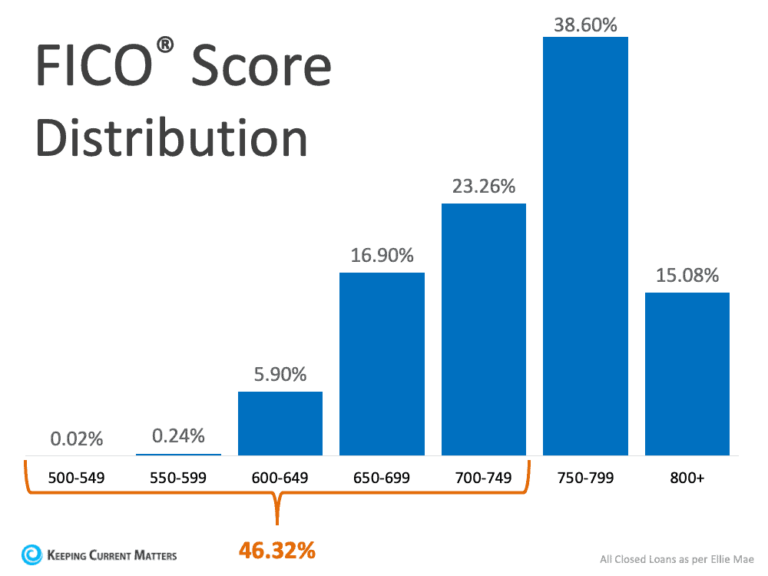

The average American has seen their credit score go up in recent years, and that’s a great sign of financial health. The higher your score goes, the better your chances of building toward a stronger financial future. As more Americans with strong credit enter the housing market, we see a natural increase in the distribution of FICO® scores for closed loans, as shown in the graph below:

If your score is below 750, it may seem like it’s not possible to qualify for a mortgage. But that’s not true! While most borrowers do have a credit score above 750, there are other factors involved in qualifying for a mortgage, and there are still options that allow people with lower scores to buy their dream home. Here’s what Experian, a global leader in consumer and business credit reporting, says:

You know that having a good credit score will give you more options and better terms when applying for a mortgage, especially when lending is tight like it is right now. But even if your score isn’t perfect, there are still ways to get into the home of your dreams,

The truth is that today’s market is full of opportunity so don’t let assumptions about whether or not your credit score is good enough put a premature end to your homeownership goals. Contact me today, your local real estate professional to discuss all of your options so you can make informed decisions about how best to achieve your dreams!

Source: www.keepingcurrentmatters.com

If you find yourself constantly checking listings online or longing for a change in scenery, it might be time to make that move. The signs that it’s time to sell your home are often subtle and hard to identify, but once you know what they are, you can make an informed decision about whether now is the right time for you. Let me help you figure out if you’re ready to sell your home or not.

Here are five signs it’s finally time to sell your home and move on:

If you’re a homeowner, you know all about the expenses that come with maintaining a property—and it can be overwhelming. You may want to sell your current home and buy one that requires less maintenance, or you may just want to get rid of the responsibility altogether and rent instead.

If you’re thinking of selling your home, it’s important to know how much money you can expect to get for it.

If you’re trying to avoid bankruptcy or foreclosure, you should only sell when you own enough equity in your home to be able to pay down your current mortgage and come out with a 20% down payment for your next home.

You’ll also want to make sure you have some extra cash in the bank to support the move. You’ll want to factor in marketing costs, the cost of staging your home, moving costs, real estate commissions, and closing costs. If you won’t have enough cash flow to be able to cover these expenses, you should consider selling your house off-market.

Having a strong understanding of your financial position will help you understand if it’s a good time for you to sell. It will also help you develop a plan after the sale, so that when you buy your next house, it will be one that works well with your overall lifestyle goals and financial situation.

When thinking of selling your home, it’s important to think about the market you’re selling in. If your neighborhood has sold fast, or if prices are going up, then it might be a good time to sell.

Real estate experts recommend selling your home if any of the following conditions are true:

• Homes in your neighborhood that have sold

• What price they have sold at

• How fast they’ve sold

• Local trends in the housing market

Once you’ve looked at factors outside of your control (like how much interest rates are), you’ll want to consider factors within your control, like budgeting and setting a price range for your home.

Selling your home is a big deal. It’s not just about the money it’s about your emotional journey as well. It’s a time of reflection and change.

You’ll have to put in time, energy, and maybe even some effort helping to prepare the home for house hunters. The negotiation process can also be emotionally taxing. You must also feel ready to declutter your home and leave behind all the memories you and your family made there. Make sure you’re emotionally ready for all of this before deciding whether or not to sell.

Always keep your goals in mind, and remember that there are a number of things you’ll want to look at when deciding whether or not to sell your house. Being ready is the most important thing, so get started on the preparations early the whole process goes faster if you’re well-prepared when it comes time to go through with it.

When you feel like you’re ready to start considering selling your home, your best bet is to consult with local professionals who can help you to understand your options or when you have questions, and their advice when they offer recommendations about what you should or shouldn’t be doing. It can save you time and money in the long term if you actually take real estate professionals into consideration from day one.

If you’re thinking of selling soon, or simply wanting to gain a better understanding of the process involved in selling a house, contact me and I will be able to help you along the way.

When it comes to buying real estate, location is everything. A great location in a “hot area” can make all the difference. I’m sure you’ve heard the saying, “Location, location, location”, and that’s especially true when it comes to real estate. Being able to afford something is one thing, but being able to maintain it and see a good return on your investment is another. For many people, buying a home is something they have badly wanted.

There is nothing more important when investing in real estate than location. Location is the number one reason to purchase a property, and the number one factor in real estate appreciation. So why is location so important? In this article I will address four main reasons why location is vital for any real estate investor and in turn these reasons should help you to identify great locations for your investment properties.

People need to stop looking at the current status of the neighborhood and start paying attention to the future of the neighborhood. This is what I call reverse-engineering the future of the location you are buying a home in.

I want to show you how to properly analyze neighborhoods, so you can make certain buying real estate will be a profitable endeavor. Buy this home now and the reward is exponential. I’ll show you how much area will be developed around this property in the next 5 years.

One of the smartest people I know once said, “Don’t buy in a good or bad neighborhood, buy in a neighborhood that you can see the future of.” This statement is so incredibly true, and so very important as well. I’m not going to try to make claim to be smarter than this person who came up with this comment, but instead I’m going to say that my goal is to convey how important it is to buy in a neighborhood that you can see the future of.

Even buyers without kids will often consider the quality of the local school district before buying a house. Why? They want their home to increase in value after they buy it, and a good school district boosts home prices.

Now you know that a good school district can have a significant effect on a home’s value. But how do you determine which public school district a home is in? The easiest way is to log onto Realtor.com. A home’s listing will include a tab for nearby schools. Open that, and you’ll see the public schools located near a property. If you click on the schools listed, it’ll bring up additional information about them, including the public school district of which they are a part.

Before you buy a house, be sure to carefully take into consideration the nearby school district as this can affect how well your home sells in the future.

Time is the most valuable asset in the world, and this is why people will always pay to save time. To be within a twenty-minute drive of work is a factor when choosing the location of a home. This is why the areas close to highways, trains, or other means of easy transportation always seem to appreciate faster than areas farther away.

If you buy a house in an area where there is no public transportation, for example, then you will have to commute by car every day. This means that your time is spent not only on the road but also looking for parking spots and paying for parking fees in some cities. This is why the areas close to highways, trains, or other means of easy transportation always seem to appreciate faster than areas farther away. The best location for easy transportation is near a major highway or public transportation.

Local amenities have a direct impact on real estate prices in the area. Grocery stores, restaurants, shopping, entertainment, are some of the top amenities people are looking for when buying a home.

Buyers want these amenities within a 5-10 minute drive and poeple love the idea of being able to walk to work, or to the grocery store, restaurants, and other local amenities. If the location of the home you’re buying is within a few miles of most of these amenities it will help raise your property value.

The most desirable home locations are the greatest determinants of home values, so when you’re looking at real estate make sure you’re also considering location. Always ensure that your real estate agent take you to all of the best neighborhoods, as prices in these areas will always be higher than those in other neighborhoods.

Land is a finite resource, so this means that there is not as much available land for building new homes or apartments as there used to be—which is why location has such a great effect on home values.

If you’re looking to buy a home as an investment property, location will always be your number one priority because you want appreciation and rentability. The better the location of your property—the easier it will be to rent out and get more money per month—and the more likely it will appreciate in value over time.

In the end, it’s a matter of personal preference. If you already live in an area and know it well, it might be easier to negotiate a deal on a home that offers you everything you need. There are certainly exceptions, but unless you’re buying your first home in an area you don’t know well, location is probably more important than the features of a house (at least as far as location relates to price). You should consider what your top priorities are when it comes to determining where you want to live.Whether that search leads you in-state or out-of-state depends on what’s most important to you. Just make sure that before making the move, the new location will be right for your needs and desires!

The decision to buy property is a big one and should be left to the professionals. I can help you locate what your home might be worth, based on comparable homes in the area. The other information I can provide will show you if the homes in the area are selling, and for what price. If you decide that you do want to sell your property at some point, we can also assist you with this process. Whether your selling a house or land, call me today to find out how I can help you make today’s property transaction a success for you.

If you’re looking to buy your first home, you’re likely balancing several factors. Because both mortgage rates and home prices have risen this year, it costs more to buy a home than it did even just a few months ago. But that doesn’t mean you have to put your plans on hold.

If you partner with a trusted real estate advisor and hone your strategy, you can navigate today’s market and find the home you’re looking for. Here are two tips to help you get started.

If you’re having trouble finding a home in your budget that checks all the boxes, it may be worth taking another look at your lists of what you want and what you really need. According to the latest First-Time Homebuyer Metro Affordability Report from NerdWallet, your wish list can have as much impact on your search as your finances:

“Your budget isn’t all that you need to be concerned about; your wish list and desired location may carry just as much weight.”

It’s all about prioritization. If you’re serious about purchasing your first home soon, be flexible in what you’re looking for to open up your pool of options. Partner with a local real estate professional to better understand what’s available in today’s market and reprioritize your wish list. Remember, making a concession now doesn’t mean you’ll never have everything on your list. After you’ve moved in, you can always add certain features to make the home your own.

Some areas may have more homes within your target price range than others, but it may require you to be flexible on your location. For example, if you’re a remote worker, you may be able to expand your search radius. As Fannie Mae explains:

“. . . continued remote work flexibility is likely giving many the ability to live farther away in more affordable areas.”

The decision to search in places with a lower cost of living could help you find a home that fits your budget and checks the most boxes off your wish list.

If you’re serious about purchasing your first home this year, revisiting your wish list and desired location can help. Work with a trusted real estate advisor to explore all the options in your local market – and beyond – so you can achieve your homeownership dreams.

Source: www.keepingcurrentmatters.com

Once you’ve applied for a mortgage to buy a home, there are a few things you may not realize could affect your home loan acceptance. While it’s tempting to buy house decorations, be careful when it comes to making any big purchases. Here are a few things you may not realize you need to avoid after applying for your home loan.

Lenders need to source your funds, and cash is difficult to track. Before you deposit any funds into your accounts, consult with your loan officer about the best manner to document your transactions.

It’s not simply home-related purchases that might cause you to lose your loan. Lenders may raise an eyebrow if you make a major buy. People who have taken on new debt have greater debt-to-income ratios (how much debt you have compared to your monthly income). Because greater ratios result in riskier loans, borrowers may no longer be able to get mortgages. Resist the need to make significant purchases, especially if they are for furniture or appliances.

When you co-sign for a loan, you hold yourself responsible for its success and payback. Higher debt-to-income ratios accompany that obligation. Even if you guarantee that you will not be making the payments, your lender must count the payments against you.

Lenders must locate and track your assets. When your accounts are consistent, this work becomes considerably easier. Speak with your loan officer before transferring any funds.

It makes no difference if it’s a new credit card or a new automobile. Your FICO® score will be affected if you have your credit report run by firms in several financial channels (mortgage, credit card, auto, etc.). Lower credit scores might affect your mortgage interest rate and potentially even your approval.

Many buyers assume that having less financing available makes them less risky and hence more likely to get accepted. This is not correct. Your length and depth of credit history (rather than just your payment history) and your total usage of credit as a percentage of available credit. Closing accounts has a negative impact on both of those aspects of your score.

To summarize, be honest with your lender about any changes. Changes in income, assets, or credit should be assessed and implemented in such a way that your house loan may still be granted. If your work or employment status has recently changed, notify your lender. Finally, before you do anything financial, it’s advisable to thoroughly disclose and discuss your goals with your loan officer.

You want everything to go as smoothly as possible with your property purchase. Remember to visit your lender before making any substantial purchases, moving your money, or making any major life changes – someone who is equipped to explain how your financial actions may effect your house loan.

Please fill out the form below and we will be contacting you shortly

with information about your home.